India’s data-centre industry has moved from infrastructure footnote to one of the fastest-growing real estate asset classes in the country and a foundational layer of the USD 1 trillion real estate economy India is targeting by 2030. Reviewing calendar year 2025, the India Real Estate Report 2026 by PropTech Pulse recorded operational capacity approaching 1.4 GW across more than 200 facilities by year-end, with a further 1.0-1.3 GW then under development a pipeline that signalled conviction, not experimentation.

A Decade of Compounding

The scale of the transformation is best seen over time. India’s total data-centre stock across the top seven cities expanded more than threefold in six to seven years, reaching nearly 16 million square feet with installed IT-load capacity of roughly 1,263 MW as of April 2025. That growth curve from around 4.8 MSF and 307 MW in 2018 – reflects a market that compounded relentlessly through the rise of cloud, AI, OTT platforms, digital payments and an internet base that crossed approximately 950 million users in 2025. The April 2025 installed base of ~1,263 MW and the ~1.4 GW year-end figure reflect capacity added over the course of the year rather than differing methodologies.

Demand With a Floor Under It

Demand is anchored by hyperscalers, fintech firms, AI infrastructure providers and cloud operators, with data-localization requirements and 5G rollout adding structural, non-discretionary demand. As the report notes, AI infrastructure spend for technology firms is largely non-discretionary – meaning the demand floor holds even through global capital tightening.

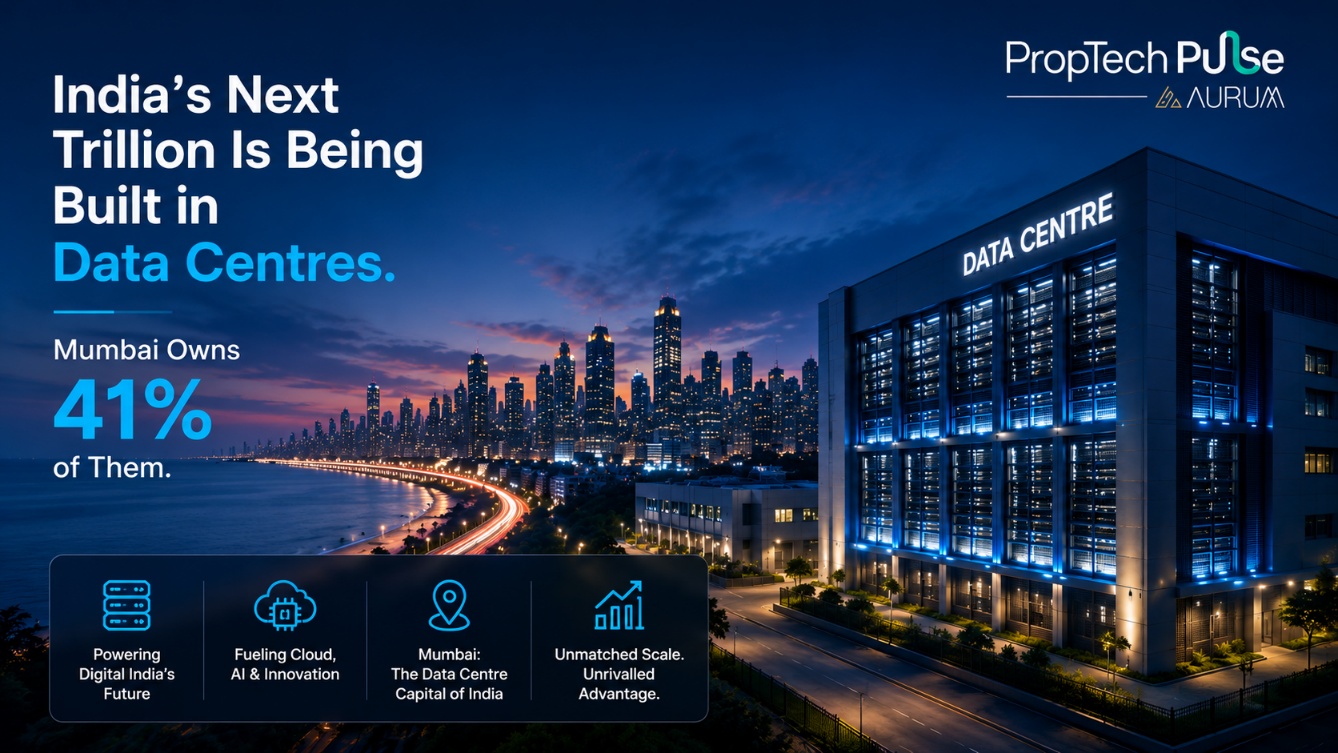

The Map: Mumbai Leads, the Field Broadens

Geographically, the market entered 2026 concentrated but broadening. Reflecting the April 2025 installed base, Mumbai MMR was India’s largest hub with 512 MW of IT load, 6.1 MSF of stock and a commanding 41% national share, driven by hyperscalers, BFSI and subsea-cable connectivity. Chennai followed with 297 MW and a 23% share, supported by a strong submarine-cable ecosystem. Delhi NCR (177 MW, 14%) emerged as a hyperscale cluster through Noida and Greater Noida, while Bengaluru (84 MW), Pune (92 MW), Hyderabad (55 MW) and Kolkata (46 MW) rounded out the top seven together accounting for the ~1,263 MW national base.

The Metros Don’t Own the Future Anymore

For the first time, India’s data-centre story is being written outside the big seven. Tier II and III cities already contribute close to 82 MW and around 1 MSF of footprint modest against the metros today but growing from a base that barely registered a few years ago. Vijayawada leads the charge, alone accounting for half the Tier II/III split, followed by Mohali and Jaipur, while a wider set of emerging hotspots Indore, Lucknow, Visakhapatnam and Coimbatore among others is beginning to draw its first serious capacity. Favourable state-level policy, enterprise digitisation, AI-driven computing demand and rising e-commerce activity beyond the metros are what’s pulling capacity inland. The metros aren’t losing their crown Tier I still hold well over 90% of national capacity but they no longer have the map to themselves, and the fastest-growing edge of it now runs through cities most investors weren’t watching.

Outlook: Crossing 2 GW in 2026

For 2026, now underway, PropTech Pulse projects operational data-centre capacity to cross approximately 2 GW, with annual investment expected to stay above USD 10-12 billion and Tier I cities continuing to account for over 90% of total capacity. Mumbai and Chennai are projected to remain the largest hubs, while Hyderabad, Pune and Bengaluru are set to see the fastest capacity expansion.

The Cost-Compression Imperative

The report also flags a cost-compression imperative shaping this next phase. Data centres are energy-intensive assets, with power typically constituting 40-60% of operating costs. Energy-price volatility and rising tariffs are accelerating the business case for renewable-energy PPAs, on-site solar and advanced cooling reframing sustainability from a compliance checkbox into an operating-margin lever.

The Investor Takeaway

For investors, the appeal is clear: a high-growth annuity asset class backed by structural, institution-grade demand. For developers, the message is to secure power, land and connectivity in the corridors where hyperscalers are already committing. India’s data-centre decade is well under way – and the capacity race is only accelerating.